IRAs & Tax-Advantaged Accounts

-

Inherited IRA Rules 2026: The SECURE Act 10-Year Rule Explained

Read more: Inherited IRA Rules 2026: The SECURE Act 10-Year Rule ExplainedIf you have inherited an IRA, the rules changed dramatically under the SECURE Act. Most non-spouse beneficiaries must now empty the account within 10 years, and since 2025 many also face annual required withdrawals along the way. Here is exactly who the 10-year rule applies to, who is exempt, how Roth IRAs differ, and how…

-

Triple Tax-Advantaged Accounts: The Complete US Guide (HSA, and What Else Counts)

Read more: Triple Tax-Advantaged Accounts: The Complete US Guide (HSA, and What Else Counts)The HSA is the only mainstream US account with three layers of tax protection. Why Roth IRAs, traditional 401(k)s, and 529 plans don’t count, what the 2026 HSA contribution limits are, and the investment-HSA strategy that turns it into a stealth retirement account.

-

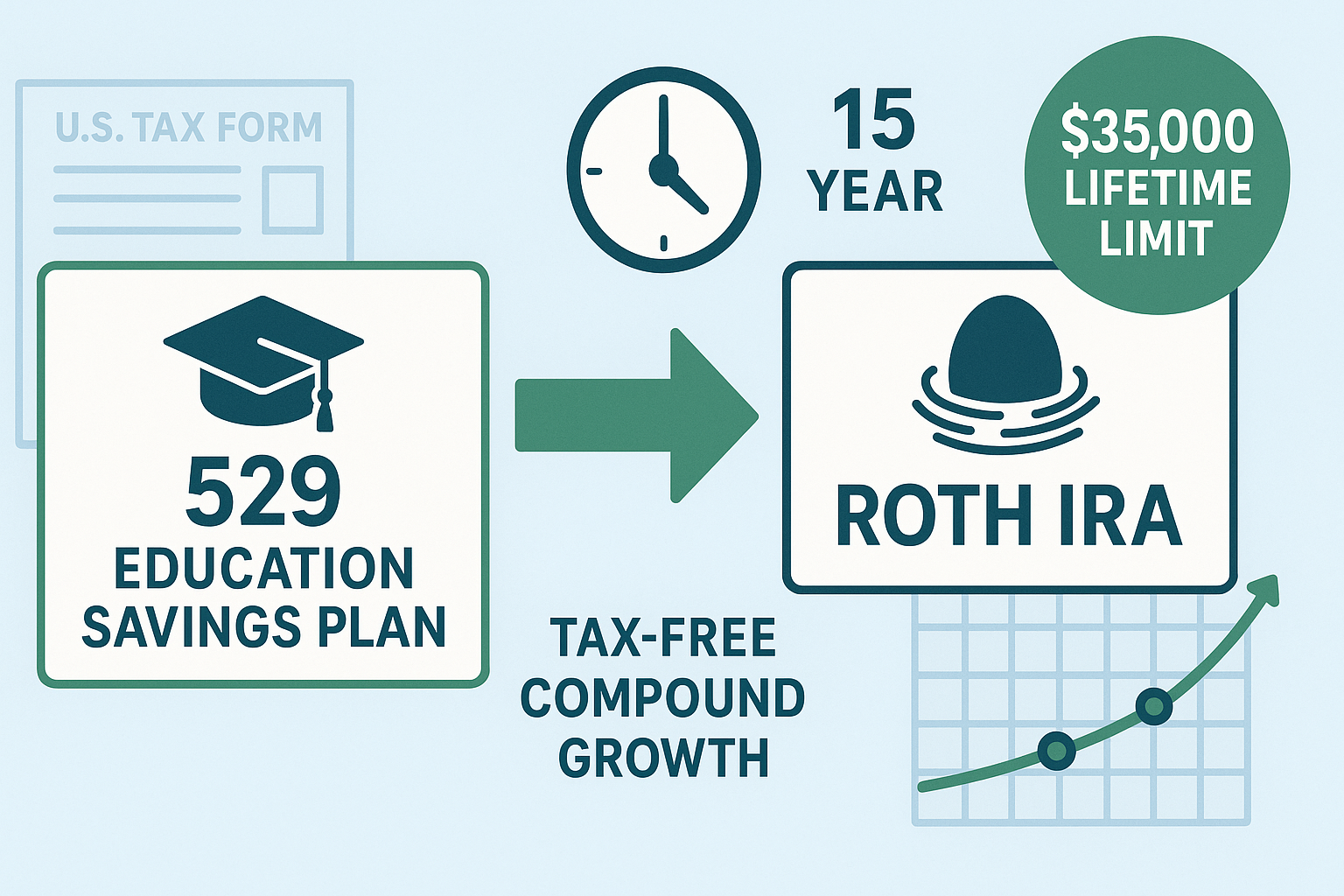

529 to Roth IRA: The 15-Year Rule Explained (2026)

Read more: 529 to Roth IRA: The 15-Year Rule Explained (2026)The most-asked question on the new 529-to-Roth IRA rollover route: how does the 15-year rule actually work? A focused FAQ covering the 15-year clock, the 5-year contribution exclusion, the $35,000 lifetime cap, the beneficiary-change uncertainty, and a worked planning example for 2026.

-

529 to Roth IRA Rollover: Complete SECURE 2.0 Guide for 2026

Read more: 529 to Roth IRA Rollover: Complete SECURE 2.0 Guide for 2026Run the 529-to-Roth IRA rollover cleanly in 2026: the 15-year rule, $35,000 lifetime cap, $7,500 annual limit, the state-tax traps that catch people, and step-by-step execution.

-

FIRE Movement: The Complete 2026 Guide to Financial Independence and Early Retirement

Read more: FIRE Movement: The Complete 2026 Guide to Financial Independence and Early RetirementFIRE planning in 2026: the ACA subsidy cliff is back, Morningstar lifted the safe withdrawal rate to 3.9%, and the IRS pushed limits higher. FI number, healthcare bridge, Roth conversion ladder, and five interactive calculators.

-

The Complete 401(k) Optimization Playbook for 2026

Read more: The Complete 401(k) Optimization Playbook for 2026Optimize your 401(k) for 2026: contribution limits up to $35,750 for ages 60-63, the mega backdoor Roth at $72,000, the Traditional-versus-Roth call, expense ratios, the new mandatory Roth catch-up for $150K+ earners, plus how to spot a bad plan and what to do at job changes. Built to add six figures to lifetime retirement savings.

-

Backdoor Roth IRA: Step-by-Step Guide (2026)

Read more: Backdoor Roth IRA: Step-by-Step Guide (2026)Income too high for a direct Roth IRA? The backdoor Roth opens the door for high earners at $7,500 a year in 2026 ($8,600 if you’re 50+). This guide walks Fidelity, Vanguard and Schwab step-by-step, runs the pro-rata math, and breaks down Form 8606 line by line.

-

Solo 401(k) Complete Guide for Self-Employed Workers (2026)

Read more: Solo 401(k) Complete Guide for Self-Employed Workers (2026)A Solo 401(k) lets the self-employed contribute up to $72,000 in 2026 ($80,000 if you’re 50+, $83,250 if you’re 60-63), well past what SEP IRAs and SIMPLE IRAs allow. This guide covers eligibility, providers, setup, contribution strategy, mega backdoor Roth, and the SECURE 2.0 Roth catch-up rule with the sole-proprietor carve-out most coverage misses.

-

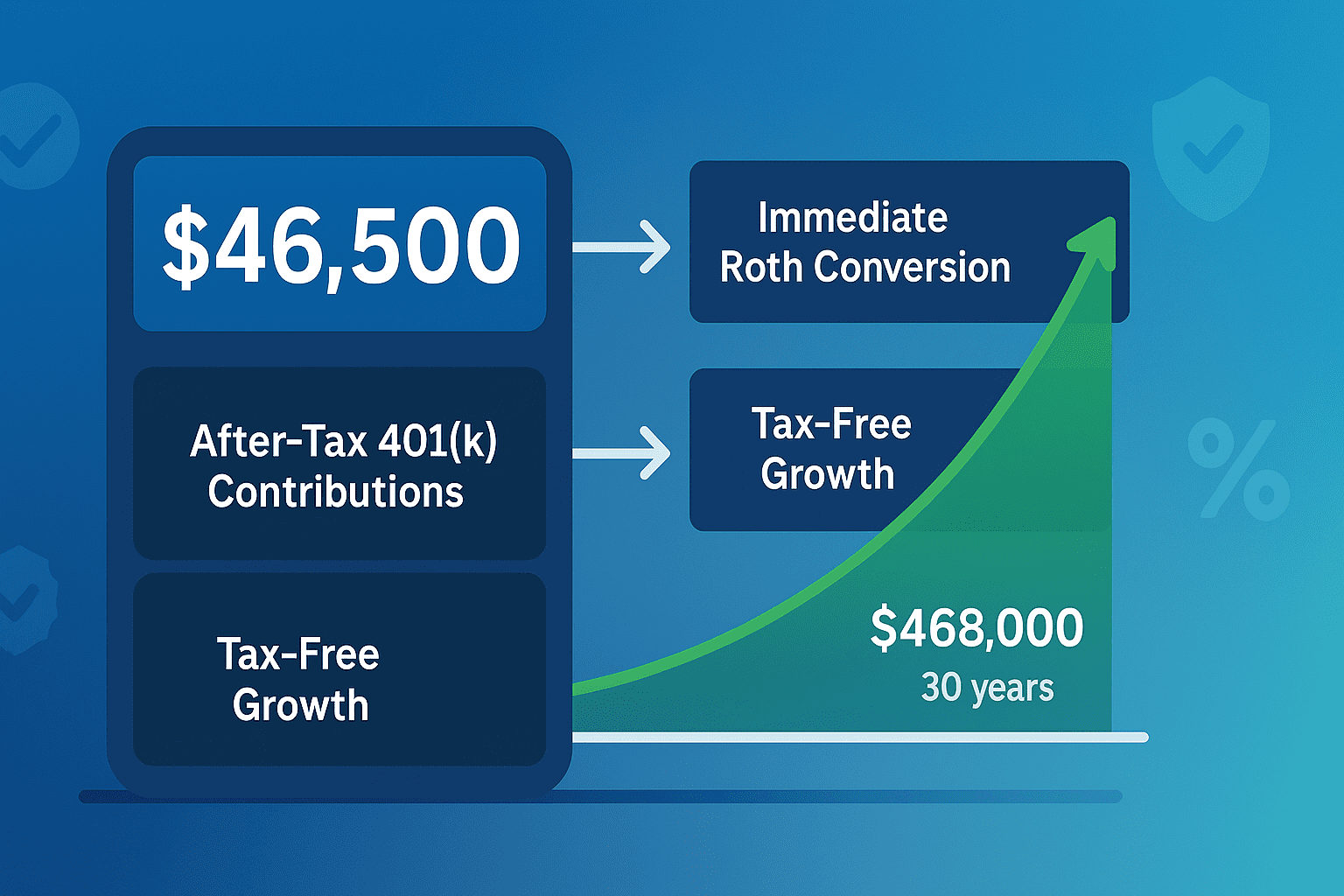

Mega Backdoor Roth: Complete Implementation Guide (2026)

Read more: Mega Backdoor Roth: Complete Implementation Guide (2026)Mega backdoor Roth lets high earners route up to $47,500 into Roth accounts in 2026. Step-by-step on eligibility, employer plan compatibility, conversion mechanics, and the SECURE 2.0 rules now phasing in.

-

HSA Investment Strategy: How to Use the Triple Tax Advantage for Retirement

Read more: HSA Investment Strategy: How to Use the Triple Tax Advantage for RetirementOnly 13% of HSA owners invest their balance, leaving the triple tax advantage on the table. A 30-year-old contributing $4,400 a year can build over $430,000 tax-free by retirement. With OBBBA’s 2026 expansions (Bronze and Catastrophic ACA plans now HSA-eligible, permanent telehealth safe harbor, Direct Primary Care arrangements compatible), HSAs are within reach of more…

Subscribe

Sign up with your email address to receive our weekly news

Latest news

- Lifetime ISA Complete Guide 2026: Bonus, Penalty and LISA vs Pension

- Inherited IRA Rules 2026: The SECURE Act 10-Year Rule Explained

- Triple Tax-Advantaged Accounts: The Complete US Guide (HSA, and What Else Counts)

- OBBBA in 2026: the SALT cap is now $40,000 and your 529 can pay $20,000 of K-12 tuition

- 529 to Roth IRA: The 15-Year Rule Explained (2026)

Categories

- Backdoor Roth (1)

- Cryptocurrency (1)

- Expat Living & Lifestyle (1)

- General Blog (13)

- Index Funds (1)

- Investing Basics (4)

- Investment Guides (6)

- Investment Platforms (1)

- Investment Strategies (12)

- Investments (2)

- IRAs & Tax-Advantaged Accounts (11)

- ISAs and Pensions (6)

- Property Investment (7)

- Real Estate Investing (3)

- Retirement Planning (19)

- Tax Strategy (16)

- Tax-Efficient Investing (4)

- UK Investing (30)

- UK Property Investment (4)