Tax Strategy

-

Inherited IRA Rules 2026: The SECURE Act 10-Year Rule Explained

Read more: Inherited IRA Rules 2026: The SECURE Act 10-Year Rule ExplainedIf you have inherited an IRA, the rules changed dramatically under the SECURE Act. Most non-spouse beneficiaries must now empty the account within 10 years, and since 2025 many also face annual required withdrawals along the way. Here is exactly who the 10-year rule applies to, who is exempt, how Roth IRAs differ, and how…

-

Triple Tax-Advantaged Accounts: The Complete US Guide (HSA, and What Else Counts)

Read more: Triple Tax-Advantaged Accounts: The Complete US Guide (HSA, and What Else Counts)The HSA is the only mainstream US account with three layers of tax protection. Why Roth IRAs, traditional 401(k)s, and 529 plans don’t count, what the 2026 HSA contribution limits are, and the investment-HSA strategy that turns it into a stealth retirement account.

-

OBBBA in 2026: the SALT cap is now $40,000 and your 529 can pay $20,000 of K-12 tuition

Read more: OBBBA in 2026: the SALT cap is now $40,000 and your 529 can pay $20,000 of K-12 tuitionTwo OBBBA provisions took effect 1 January 2026 and are reshaping US tax planning for the 2026 return. The SALT deduction cap jumps from $10,000 to $40,000 for filers below $500,500 MAGI. The 529 K-12 limit doubles to $20,000 per student and now covers tutoring, books, and credential programs.

-

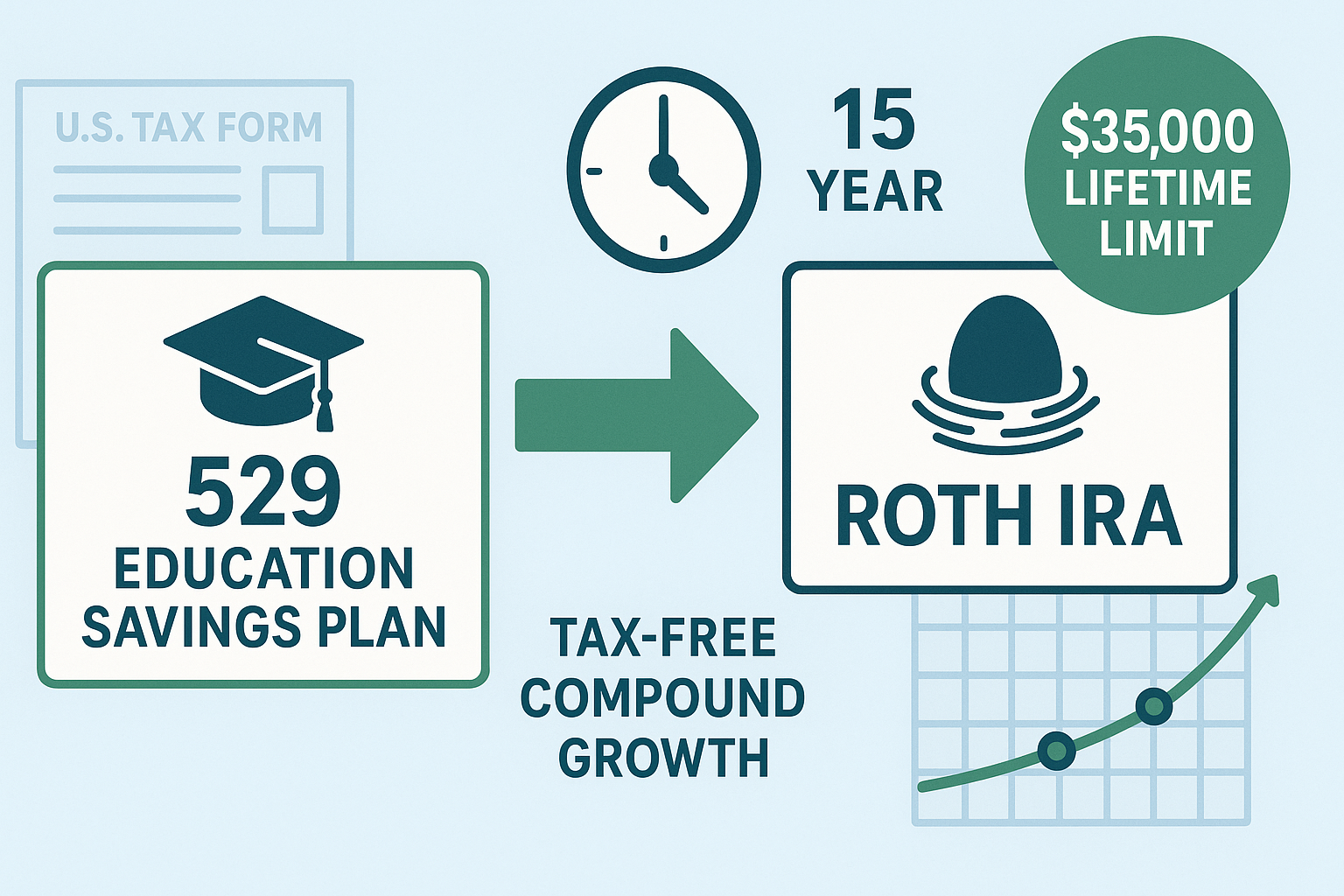

529 to Roth IRA: The 15-Year Rule Explained (2026)

Read more: 529 to Roth IRA: The 15-Year Rule Explained (2026)The most-asked question on the new 529-to-Roth IRA rollover route: how does the 15-year rule actually work? A focused FAQ covering the 15-year clock, the 5-year contribution exclusion, the $35,000 lifetime cap, the beneficiary-change uncertainty, and a worked planning example for 2026.

-

Best Cash ISA Rates in May 2026: a Companion to the £12,000 Under-65 Cap Guide

Read more: Best Cash ISA Rates in May 2026: a Companion to the £12,000 Under-65 Cap GuideShort companion piece to the £12,000 Cash ISA cap guide. The best-buy easy-access and fixed-rate Cash ISA rates as of mid-May 2026, with notes on the new NS&I British Savings Bonds, FSCS protection, and how to use the full £20,000 allowance this tax year before the under-65 cap arrives in April 2027.

-

Dividend Tax Rates Have Gone Up: What the New 2026/27 Rates Mean for Investors Holding Shares Outside an ISA

Read more: Dividend Tax Rates Have Gone Up: What the New 2026/27 Rates Mean for Investors Holding Shares Outside an ISAFrom 6 April 2026, dividend tax rates rose by 2pp in the basic and higher rate bands. From April 2027, savings income tax rates rise too. What the new numbers actually mean for investors holding dividend-paying shares in a General Investment Account, and how the gap between in-ISA and out-of-ISA returns has widened.

-

Making Tax Digital for Income Tax: Who Must Sign Up Now, What Happens If You Don’t, and What the Penalty-Free Year Really Means

Read more: Making Tax Digital for Income Tax: Who Must Sign Up Now, What Happens If You Don’t, and What the Penalty-Free Year Really MeansMTD for Income Tax is now in force. Sole traders and landlords with qualifying income above £50,000 must keep digital records and submit quarterly updates, with the first deadline on 7 August 2026. The threshold drops to £30,000 in 2027 and £20,000 in 2028. Here is exactly who is in scope, how the soft-landing year…

-

Pension Inheritance Tax 2027: UK Estate Planning Guide

Read more: Pension Inheritance Tax 2027: UK Estate Planning GuideFrom 6 April 2027, unspent UK pension pots fall into the IHT estate. What’s changing, who’s hit hardest, and the 6 planning moves to consider before the 2027 deadline.

-

529 to Roth IRA Rollover: Complete SECURE 2.0 Guide for 2026

Read more: 529 to Roth IRA Rollover: Complete SECURE 2.0 Guide for 2026Run the 529-to-Roth IRA rollover cleanly in 2026: the 15-year rule, $35,000 lifetime cap, $7,500 annual limit, the state-tax traps that catch people, and step-by-step execution.

-

Tax-Loss Harvesting Strategy Guide (2026): Complete US & UK Implementation for DIY Investors

Read more: Tax-Loss Harvesting Strategy Guide (2026): Complete US & UK Implementation for DIY InvestorsCrystallise capital losses without tripping the US wash-sale rule or the UK 30-day bed-and-breakfasting restriction. 2026 figures, the ETF pairs that actually work, when automated services beat DIY, and the ten mistakes that quietly destroy most harvesters’ tax benefit.

Subscribe

Sign up with your email address to receive our weekly news

Latest news

- Inherited IRA Rules 2026: The SECURE Act 10-Year Rule Explained

- Triple Tax-Advantaged Accounts: The Complete US Guide (HSA, and What Else Counts)

- OBBBA in 2026: the SALT cap is now $40,000 and your 529 can pay $20,000 of K-12 tuition

- 529 to Roth IRA: The 15-Year Rule Explained (2026)

- How Much Could £1,000 Invested Actually Earn? Worked Returns for UK Beginners 2026

Categories

- Backdoor Roth (1)

- Cryptocurrency (1)

- Expat Living & Lifestyle (1)

- General Blog (13)

- Index Funds (1)

- Investing Basics (4)

- Investment Guides (6)

- Investment Platforms (1)

- Investment Strategies (12)

- Investments (2)

- IRAs & Tax-Advantaged Accounts (11)

- ISAs and Pensions (5)

- Property Investment (7)

- Real Estate Investing (3)

- Retirement Planning (18)

- Tax Strategy (16)

- Tax-Efficient Investing (3)

- UK Investing (29)

- UK Property Investment (4)