Retirement Planning

-

Triple Tax-Advantaged Accounts: The Complete US Guide (HSA, and What Else Counts)

Read more: Triple Tax-Advantaged Accounts: The Complete US Guide (HSA, and What Else Counts)The HSA is the only mainstream US account with three layers of tax protection. Why Roth IRAs, traditional 401(k)s, and 529 plans don’t count, what the 2026 HSA contribution limits are, and the investment-HSA strategy that turns it into a stealth retirement account.

-

OBBBA in 2026: the SALT cap is now $40,000 and your 529 can pay $20,000 of K-12 tuition

Read more: OBBBA in 2026: the SALT cap is now $40,000 and your 529 can pay $20,000 of K-12 tuitionTwo OBBBA provisions took effect 1 January 2026 and are reshaping US tax planning for the 2026 return. The SALT deduction cap jumps from $10,000 to $40,000 for filers below $500,500 MAGI. The 529 K-12 limit doubles to $20,000 per student and now covers tutoring, books, and credential programs.

-

529 to Roth IRA: The 15-Year Rule Explained (2026)

Read more: 529 to Roth IRA: The 15-Year Rule Explained (2026)The most-asked question on the new 529-to-Roth IRA rollover route: how does the 15-year rule actually work? A focused FAQ covering the 15-year clock, the 5-year contribution exclusion, the $35,000 lifetime cap, the beneficiary-change uncertainty, and a worked planning example for 2026.

-

From rate cuts to a rate hike: what May’s jobs report and Warsh’s first FOMC mean for US savers, borrowers and retirees

Read more: From rate cuts to a rate hike: what May’s jobs report and Warsh’s first FOMC mean for US savers, borrowers and retireesMay’s +172,000 jobs report flipped the market from pricing Federal Reserve rate cuts to pricing a hike. Here is what Kevin Warsh’s first FOMC meeting on 16-17 June means for US savers, borrowers, and retirees, and why the Fed’s balance sheet matters as much as the rate.

-

FCA Targeted Support 2026: Your Pension Platform Can Now Nudge You — What That Means

Read more: FCA Targeted Support 2026: Your Pension Platform Can Now Nudge You — What That MeansThe FCA’s new targeted support regime is live from 6 April 2026. What it lets pension platforms do, what it doesn’t replace, and how to use it as a UK saver.

-

Pension Inheritance Tax 2027: UK Estate Planning Guide

Read more: Pension Inheritance Tax 2027: UK Estate Planning GuideFrom 6 April 2027, unspent UK pension pots fall into the IHT estate. What’s changing, who’s hit hardest, and the 6 planning moves to consider before the 2027 deadline.

-

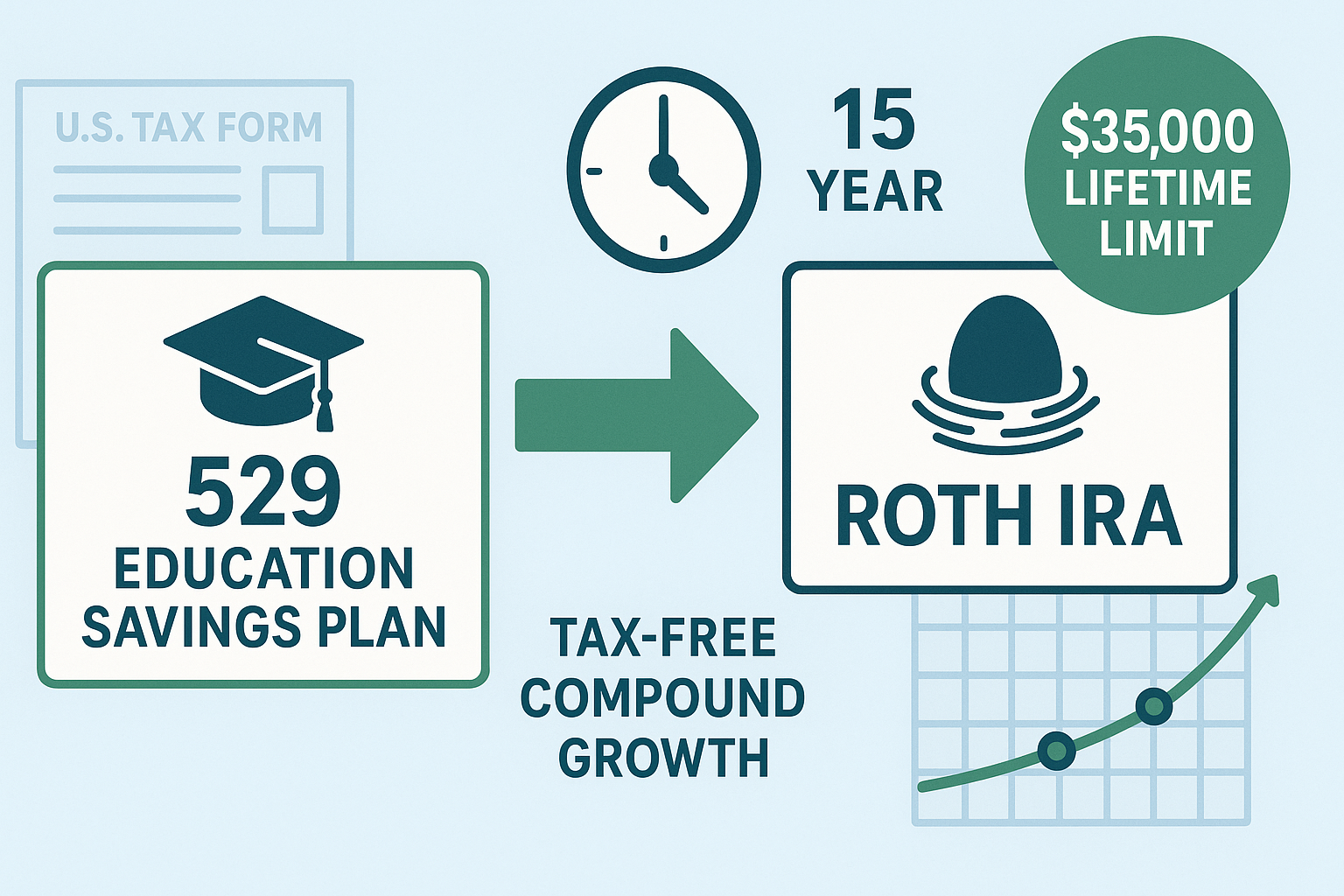

529 to Roth IRA Rollover: Complete SECURE 2.0 Guide for 2026

Read more: 529 to Roth IRA Rollover: Complete SECURE 2.0 Guide for 2026Run the 529-to-Roth IRA rollover cleanly in 2026: the 15-year rule, $35,000 lifetime cap, $7,500 annual limit, the state-tax traps that catch people, and step-by-step execution.

-

FIRE Movement: The Complete 2026 Guide to Financial Independence and Early Retirement

Read more: FIRE Movement: The Complete 2026 Guide to Financial Independence and Early RetirementFIRE planning in 2026: the ACA subsidy cliff is back, Morningstar lifted the safe withdrawal rate to 3.9%, and the IRS pushed limits higher. FI number, healthcare bridge, Roth conversion ladder, and five interactive calculators.

-

The Complete 401(k) Optimization Playbook for 2026

Read more: The Complete 401(k) Optimization Playbook for 2026Optimize your 401(k) for 2026: contribution limits up to $35,750 for ages 60-63, the mega backdoor Roth at $72,000, the Traditional-versus-Roth call, expense ratios, the new mandatory Roth catch-up for $150K+ earners, plus how to spot a bad plan and what to do at job changes. Built to add six figures to lifetime retirement savings.

-

Backdoor Roth IRA: Step-by-Step Guide (2026)

Read more: Backdoor Roth IRA: Step-by-Step Guide (2026)Income too high for a direct Roth IRA? The backdoor Roth opens the door for high earners at $7,500 a year in 2026 ($8,600 if you’re 50+). This guide walks Fidelity, Vanguard and Schwab step-by-step, runs the pro-rata math, and breaks down Form 8606 line by line.

Subscribe

Sign up with your email address to receive our weekly news

Latest news

- Triple Tax-Advantaged Accounts: The Complete US Guide (HSA, and What Else Counts)

- OBBBA in 2026: the SALT cap is now $40,000 and your 529 can pay $20,000 of K-12 tuition

- 529 to Roth IRA: The 15-Year Rule Explained (2026)

- How Much Could £1,000 Invested Actually Earn? Worked Returns for UK Beginners 2026

- From rate cuts to a rate hike: what May’s jobs report and Warsh’s first FOMC mean for US savers, borrowers and retirees

Categories

- Backdoor Roth (1)

- Cryptocurrency (1)

- Expat Living & Lifestyle (1)

- General Blog (13)

- Index Funds (1)

- Investing Basics (4)

- Investment Guides (6)

- Investment Platforms (1)

- Investment Strategies (12)

- Investments (2)

- IRAs & Tax-Advantaged Accounts (10)

- ISAs and Pensions (5)

- Property Investment (7)

- Real Estate Investing (3)

- Retirement Planning (17)

- Tax Strategy (15)

- Tax-Efficient Investing (3)

- UK Investing (29)

- UK Property Investment (4)